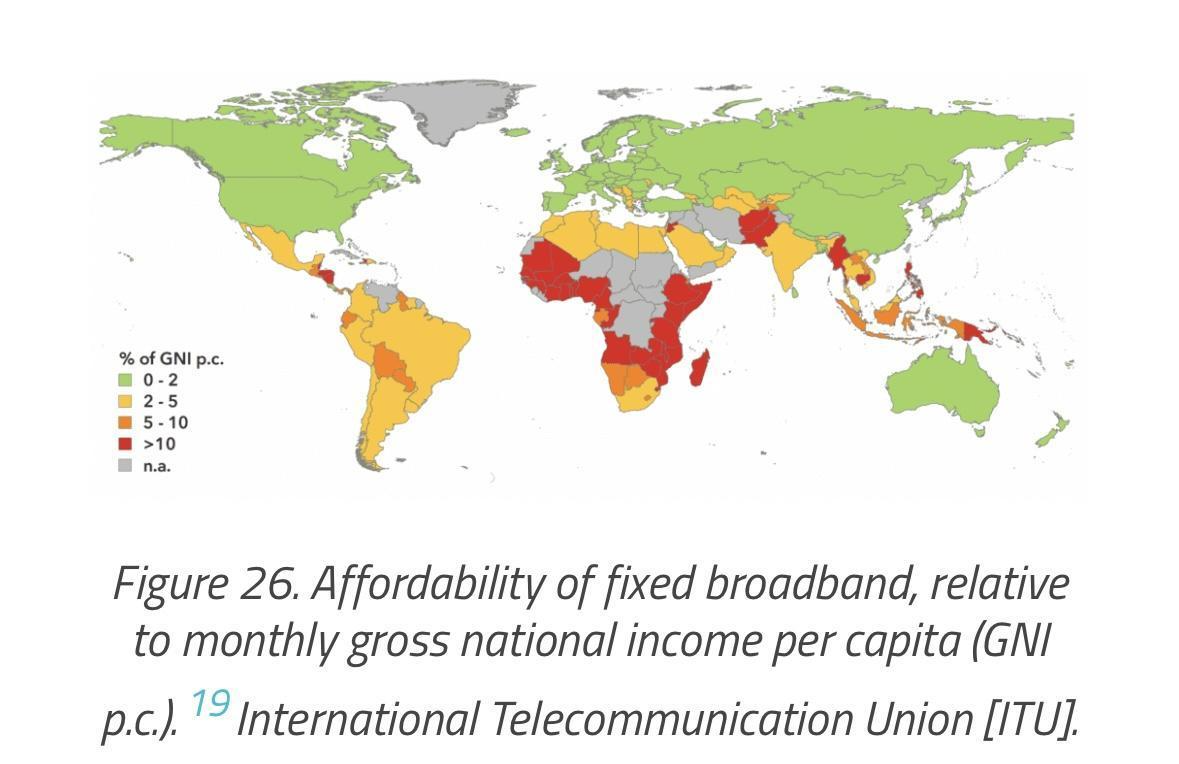

- In Africa, the affordability of broadband is driven by competitive telecom markets, submarine cable investments, and government-backed pricing reforms expanding access.

- Falling costs are accelerating digital adoption, enabling growth in mobile banking, streaming, and e-commerce while reducing reliance on costly mobile data bundles.

- Egypt, Sudan, and Tunisia stand out for affordable broadband, each adopting different models.

Deep Dive!!

Lagos, Nigeria, Wednesday, October 1 – Africa’s digital landscape is undergoing a transformative shift, with broadband affordability emerging as a critical driver of connectivity. Countries across the continent are reporting some of the lowest monthly broadband costs worldwide, positioning Africa as a leader in affordable internet access.

This progress comes at a pivotal time whereinternet penetration rates are climbing steadily, supported by rising smartphone adoption and an urban population that increasingly depends on digital services for education, commerce, and communication.

For governments , corporate workplaces, ordinary businesses and homes , affordable broadband is no longer a luxury but the foundation of inclusive economic growth, unlocking pathways for e-learning, fintech expansion, and e-commerce integration.

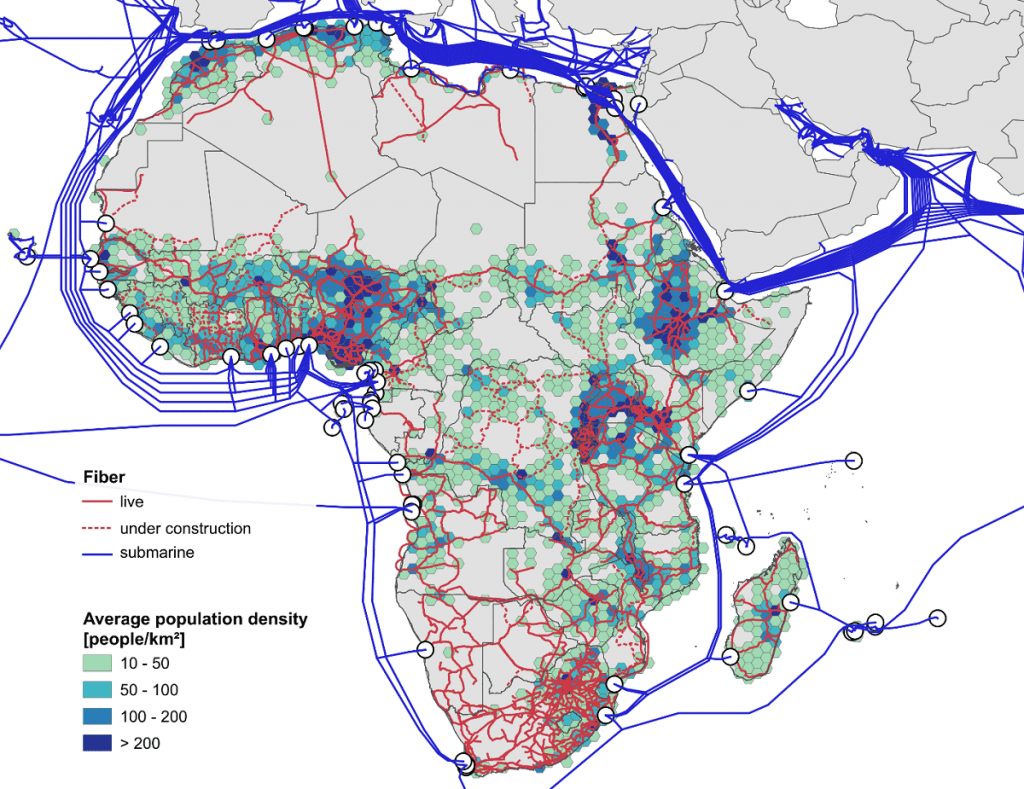

The forces behind this affordability trend are structural and deliberate. Aggressive investment in undersea cables, such as Equiano and 2Africa, coupled with cross-border fiber optic expansions, has slashed wholesale data costs by as much as 70% in certain markets.

Most African governments are also rolling out national broadband strategies that reduce taxes on infrastructure equipment and encourage public-private partnerships, ensuring wider last-mile coverage. At the same time, competition has intensified as established telcos, agile regional providers, and disruptive low-cost ISPs all battle for market share, pushing consumer prices lower.

The resulting broadband market is not uniform but rather a mosaic of innovation and adaptation.

Some states prioritize affordability through subsidies and entry-level packages, while others lean on private sector efficiency to keep costs competitive. Fintech adoption, online education platforms, and digital government services are rapidly rising in markets where broadband affordability improves, creating feedback loops that fuel further demand.

This diversity is a true testament of a central truth: Africa’s broadband success is not about a single model but about the convergence of infrastructure, policy, and market dynamics.

It’s against this background that, featuring in Market intellengece this week is a comprehensive list of the top ten African countries where broadband affordability is reshaping digital access, economic opportunity, and the everyday lives of millions.

10. Liberia

Liberia entered Africa’s top ten most affordable broadband markets with an average subscription price of $24 per month and a per-megabit cost of $7.70. This progress stems largely from the country’s connection to the Africa Coast to Europe (ACE) submarine cable, which landed in Monrovia in 2012 and remains a cornerstone of its digital backbone. Before ACE, Liberia relied heavily on expensive satellite links that restricted speed and affordability. The submarine link opened the door for international bandwidth capacity and helped local operators reduce wholesale internet costs, making consumer broadband far more attainable.

Liberia’s affordability also reflects its mobile-first broadband model. With fixed-line penetration still under 1%, most citizens depend on 3G and 4G mobile networks operated by Lonestar Cell MTN and Orange Liberia. Both companies have expanded coverage beyond Monrovia into rural counties, introducing competitive pricing bundles that allow subscribers to purchase internet in small, flexible units. The rivalry between these operators is a significant factor in keeping broadband within reach for households and small businesses, who often combine mobile broadband with affordable smartphones for work, study, and entertainment.

On the policy front, Liberia’s government has worked to attract international donor support for connectivity expansion. Programs funded by the World Bank and USAID are helping extend backbone infrastructure inland, reducing reliance on Monrovia’s coastal cable access. Meanwhile, the National ICT Policy (2019–2024) prioritizes rural connectivity and digital literacy, with pilot projects for community internet centers in underserved areas. Despite persistent challenges such as electricity shortages and limited last-mile fiber, Liberia’s steady decline in broadband costs shows how a blend of submarine infrastructure, operator competition, and global partnerships is creating a more inclusive digital economy for its 5 million citizens.

9. Nigeria

Nigeria ranks among Africa’s more affordable broadband markets, with an average monthly subscription of $22 and a per-megabit cost of $0.72. The country’s relatively low per-megabit pricing is tied to its vast international bandwidth capacity, anchored by multiple submarine cables, including Glo-1, MainOne, and WACS, that land along the Lagos coastline. These cables, owned or co-owned by Nigerian firms, have allowed local providers to bypass high international transit costs and directly access global networks. Combined with a rapidly expanding domestic fiber backbone driven by private sector leaders such as MainOne (now part of Equinix) and IHS Towers, Nigeria has been able to distribute bandwidth more efficiently to major urban hubs like Lagos, Abuja, and Port Harcourt.

Competition among operators is another key factor in Nigeria’s broadband affordability. The market is dominated by MTN Nigeria, Airtel, Globacom, and 9mobile, with MTN and Airtel commanding the largest share. Their constant rivalry has resulted in aggressive pricing, bundled data offers, and innovative mobile broadband packages aimed at attracting Nigeria’s young, tech-savvy population. The National Broadband Plan (2020–2025) has also been instrumental, setting targets for 70% broadband penetration and incentivizing providers to extend services into semi-urban and rural areas. Policies such as the harmonization of Right-of-Way (RoW) charges across states have helped reduce deployment costs for fiber, making it cheaper to deliver last-mile connections.

Nigeria, which is home to over 220 million people, also plays a unique role in shaping its broadband economy. With the largest digital consumer base on the continent, providers benefit from economies of scale that allow them to spread infrastructure costs across millions of subscribers. The government has backed this momentum through public-private partnerships, such as collaborations with Google’s Equiano subsea cable, which went live in 2023 and promises to further reduce latency and wholesale internet costs. While persistent challenges remain, especially in powering infrastructure during Nigeria’s chronic electricity shortages, the country’s combination of abundant undersea bandwidth, a competitive telecoms market, and regulatory reform has positioned it as one of Africa’s leaders in affordable broadband access.

8. Algeria

Algeria recorded an average broadband subscription cost of $21 per month and a per-megabit cost of $0.57, placing it among the continent’s most affordable markets. This achievement stems from the country’s long-standing investment in state-led digital infrastructure, particularly through Algérie Télécom, the national operator that dominates the fixed broadband sector. The backbone of Algeria’s affordability lies in its extensive fiber-optic network, built to connect major cities and regional centers, reducing dependency on international carriers for domestic data traffic. Algeria also benefits from multiple submarine cable landings along its Mediterranean coastline, which anchor the country firmly into Europe’s high-capacity internet corridors. These connections lower wholesale costs and provide redundancy, keeping bandwidth relatively stable even during regional outages.

The government has played a central role in shaping Algeria’s broadband market, particularly through its policy of state-subsidized infrastructure development. Large-scale national projects like the “Algeria Broadband” program have been rolled out to ensure that underserved areas receive access, even where private providers may find it commercially unviable. By controlling much of the infrastructure cost through public funding, the state has kept retail broadband prices moderate compared to peer economies with similar income levels. Moreover, Algeria’s policy of benchmarking local tariffs against international affordability standards has encouraged operators to maintain competitive pricing. Unlike purely market-driven models, Algeria’s hybrid system blends regulation and subsidy to keep broadband within reach of ordinary households.

Algeria’s affordability also reflects the role of regional positioning and socio-economic priorities. With a population of over 44 million, demand for digital services is expanding rapidly, particularly in e-government, education, and e-commerce. The government has made internet access a cornerstone of its digital transformation strategy, emphasizing affordability as a tool to stimulate national productivity and youth employment. Algeria’s location on the MedRing project, a fiber-optic network linking Mediterranean nations, further enhances its access to international bandwidth at reduced costs. While critics often point to limited competition and slower speeds compared to some African peers, Algeria’s structural advantages in submarine connectivity, coupled with sustained public investment, explain why the country continues to deliver relatively low-cost broadband access in North Africa.

7. Libya

Libya reported an average broadband cost of $19 per month, with a per-megabit price of $4.48, making it one of the cheapest markets in North Africa despite its ongoing political and economic challenges. This affordability is linked to the country’s legacy infrastructure and high-capacity international connections established before the civil conflicts. Libya has access to multiple submarine cables along the Mediterranean, which connect it directly to Europe and help reduce international bandwidth costs. Even with periods of disruption in governance, the presence of these cables has ensured that Libya maintains lower wholesale costs than many of its regional neighbors, translating into competitive end-user pricing.

The country’s telecom sector is dominated by Libya Telecom & Technology (LTT), the state-owned operator responsible for both wholesale and retail broadband services. Because of its central role, LTT sets relatively standardized pricing across the market, limiting excessive fluctuations and preventing steep costs. Unlike many African states where broadband relies heavily on mobile data, Libya has a relatively higher share of fixed broadband connections, supported by its urban concentration and legacy fiber networks laid in the early 2000s. This fixed infrastructure base reduces reliance on costly mobile packages and contributes to lower average monthly broadband bills for households and small businesses.

Government strategies in recent years have also sought to leverage broadband as a stabilizing force in the economy. Programs under the Libyan Post, Telecommunication, and Information Technology Company (LPTIC) have targeted upgrades to the fiber backbone and sought international partnerships to restore damaged infrastructure. Digital access has been prioritized for universities, public institutions, and essential services to ensure continuity despite political instability. While speed and service quality remain uneven due to security disruptions, Libya’s broadband affordability highlights the long-term value of infrastructure built during earlier stable periods and underscores the importance of maintaining international bandwidth access even in fragile states.

6. Ethiopia

Ethiopia’s average broadband subscription cost stood at $18 per month, with a per-megabit cost of $2.02. While slightly higher than some North African peers, Ethiopia’s position among Africa’s ten most affordable broadband markets reflects deliberate reforms in its telecom sector. For decades, the market was dominated exclusively by Ethio Telecom, the state monopoly that controlled pricing and infrastructure. The government’s decision to liberalize the sector, granting licenses to private operators such as Safaricom Ethiopia, has begun reshaping broadband dynamics. Increased competition has already pushed tariffs downward, particularly in urban centers, while ongoing investments in 4G and pilot 5G networks have expanded capacity to support more affordable data packages.

The backbone of Ethiopia’s broadband affordability lies in its strategic investments in fiber-optic expansion and international connectivity. The government prioritized extending fiber links to industrial parks, universities, and administrative hubs, ensuring that high-capacity internet supports economic development. Internationally, Ethiopia’s access to the Eastern Africa Submarine Cable System (EASSy) and the Djibouti Data MENA cable via terrestrial fiber routes provides essential redundancy and reduces reliance on costly satellite bandwidth. By tapping into Djibouti’s role as a regional cable landing hub, Ethiopia secures stable and lower-cost international bandwidth, which operators then pass on to consumers through more competitive pricing.

Policy reforms have also placed affordability at the center of Ethiopia’s broader Digital Ethiopia 2025 strategy. This roadmap prioritizes internet access as a driver of innovation, financial inclusion, and service delivery, particularly in agriculture and small-scale manufacturing. By promoting public-private partnerships and encouraging operators to expand rural coverage, the government aims to lower connectivity costs beyond Addis Ababa and other major cities. The presence of development partners such as the World Bank in supporting rural broadband rollout has also eased infrastructure costs. Although Ethiopia still faces challenges of uneven penetration and occasional service disruptions, its placement in the top tier of affordable broadband markets reflects the success of gradual liberalization, international bandwidth access, and a clear national vision for digital transformation.

5. Tunisia

Tunisia’s average broadband subscription cost was $15 per month, with a per-megabit price of $0.67, securing its place among Africa’s most affordable internet markets. This achievement is closely tied to Tunisia’s longstanding strategy of investing in both fiber and ADSL infrastructure, which has given it one of the most developed broadband backbones in North Africa. Operators like Tunisie Télécom, Ooredoo Tunisia, and Orange Tunisia compete actively in the market, creating downward pressure on prices while improving coverage and reliability. With a relatively high fixed broadband penetration rate compared to many African countries, Tunisian households benefit from stable, wired connections that help keep monthly costs consistent and predictable.

The country’s affordability also reflects its integration into Mediterranean digital networks. Tunisia is directly connected to Europe through multiple submarine cable systems, including the Didon and Hannibal cables, which provide high-capacity links at lower wholesale costs. These international gateways allow Tunisian operators to access abundant bandwidth, which is then distributed across both urban and semi-urban areas at competitive retail prices. Moreover, the government’s commitment to liberalizing the telecoms sector has encouraged private operators to expand fiber-to-the-home (FTTH) and fixed-wireless solutions, ensuring that affordability extends beyond the capital into secondary cities.

Tunisia’s digital development strategy has placed broadband access at the core of its innovation-driven economic reforms. Policies under the National Strategic Plan for Digital Tunisia 2025 emphasize ICT as a growth sector, with subsidies and tax incentives directed at expanding rural connectivity and supporting local start-ups in e-commerce, fintech, and e-learning. By linking broadband affordability with broader goals of employment generation and service modernization, Tunisia has positioned internet access as both a social good and an economic enabler. While regional inequalities in access still exist, the combination of competitive pricing, robust submarine connectivity, and state-backed policy alignment explains why Tunisia remains one of the continent’s leaders in affordable broadband provision.

4. Republic of the Congo

The Republic of the Congo offered broadband at an average cost of $13 per month, with a strikingly low per-megabit price of $0.12, one of the most competitive figures on the continent. This remarkable affordability is anchored in the country’s heavy reliance on submarine cable infrastructure, particularly the West Africa Cable System (WACS) and the Central African Backbone (CAB) project, which have significantly reduced wholesale internet costs. By leveraging these international gateways, Congo has been able to keep consumer-level broadband pricing accessible despite its relatively small market size. Urban centers like Brazzaville and Pointe-Noire, directly linked to these backbones, enjoy the most affordable packages, which explains the country’s strong ranking.

The broadband market in Congo is shaped by a mix of state involvement and private competition, which together encourage both price stability and service expansion. The government, through the Regulatory Agency for Post and Electronic Communications (ARPCE), has promoted policies that prevent excessive tariff hikes while supporting the entry of private operators like MTN Congo and Airtel. This has fostered a degree of competition that pushes providers to offer attractive bundles and reduce costs to capture market share. In addition, the state has invested in national fiber-optic links connecting remote towns to urban hubs, helping distribute international bandwidth more evenly across the country.

Congo’s broader digital transformation agenda has also contributed to affordability. Initiatives such as the “Congo Digital 2025” strategy have prioritized internet access as a national development goal, linking broadband to education, healthcare, and e-government services. Partnerships with institutions like the World Bank and the African Development Bank under the CAB project have further strengthened the country’s connectivity, ensuring that affordability is not limited to major cities alone. By aligning infrastructure development with policy frameworks and regional cooperation, the Republic of the Congo has created a structural foundation that allows it to deliver some of the most competitive broadband prices in Africa.

3. Zimbabwe

Zimbabwe ranked third in Africa’s broadband affordability index, with an average monthly subscription cost of $10 and a per-megabit price of $0.38. This pricing reflects years of deliberate sectoral reforms, including a push to expand national fiber connectivity through the Zimbabwe National Backbone Fiber Project. The country’s main operators, Liquid Intelligent Technologies, TelOne, and Econet Wireless, have invested heavily in terrestrial fiber routes that link Zimbabwe to undersea cables through neighboring Mozambique and South Africa. These connections reduce reliance on costly satellite bandwidth and enable service providers to secure wholesale capacity at more competitive rates, a key factor behind the relatively low consumer-level pricing.

The structure of Zimbabwe’s telecoms market also plays a role in keeping broadband affordable. The Postal and Telecommunications Regulatory Authority of Zimbabwe (POTRAZ) has introduced price ceilings on data tariffs, ensuring that operators do not pass on disproportionate costs to consumers even during economic fluctuations. In addition, the market benefits from the presence of Liquid Intelligent Technologies, which has built one of Africa’s largest independent fiber networks and uses economies of scale to deliver affordable internet packages. Competition among major players has further accelerated reductions in broadband prices, with providers frequently offering bundled data, voice, and digital services to attract customers.

Zimbabwe’s progress is further supported by national policy alignment. The government’s National ICT Policy 2025 emphasizes connectivity as a pillar of socio-economic recovery and modernization. Projects targeting e-learning, e-health, and fintech platforms are designed around affordable broadband access, ensuring that digital transformation is not confined to urban elites but reaches rural populations as well. Development partners have also supported infrastructure rollouts, particularly in under-connected regions, to widen access while keeping costs stable. Despite broader economic volatility, Zimbabwe’s ability to sustain one of Africa’s lowest broadband tariffs demonstrates the effectiveness of combining regulatory oversight, infrastructure investment, and regional bandwidth integration.

2. Egypt

Egypt ranks second in Africa for broadband affordability, with an average monthly subscription cost of $8 and a per-megabit rate of just $0.17. These figures position the country not only as one of the most affordable in Africa but also as competitive on a global scale. The affordability is largely linked to Egypt’s well-developed telecommunications infrastructure and its strategic position as a landing hub for multiple subsea cables connecting Africa, Europe, and Asia. By hosting over a dozen international cable systems, including SEA-ME-WE 5, AAE-1, and the Europe India Gateway, Egypt secures abundant international bandwidth, which lowers wholesale costs for service providers and, in turn, reduces consumer tariffs.

The country’s telecom sector is anchored by Telecom Egypt, which manages much of the international bandwidth and fiber backbone, while private operators such as Vodafone Egypt, Orange Egypt, and Etisalat Misr compete vigorously in the retail broadband market. This competition has played a decisive role in bringing down prices. Operators frequently offer affordable home broadband packages alongside mobile internet services, ensuring coverage for both urban and semi-urban populations. The growth of 4G services and preparations for 5G rollout have further diversified access channels, allowing millions to connect at lower entry costs. Additionally, government incentives, such as spectrum allocations and tax relief for digital infrastructure projects, have created a favorable environment for sustained broadband expansion.

Beyond infrastructure and competition, Egypt’s policy direction has also supported broadband affordability. The Digital Egypt Strategy, launched by the Ministry of Communications and Information Technology, emphasizes inclusive digital transformation by prioritizing affordable internet for households, schools, and businesses. Public–private partnerships have driven significant fiber-to-the-home deployments in cities like Cairo and Alexandria, while community connectivity projects have extended affordable services to rural areas in Upper Egypt. International partnerships with institutions like the World Bank have provided funding for digital inclusion initiatives, ensuring that affordability is matched by accessibility. Together, these efforts have placed Egypt at the forefront of Africa’s broadband affordability landscape, showcasing how infrastructure, policy, and market forces can align to achieve sustainable outcomes.

1. Sudan

Sudan holds the top position in Africa’s broadband affordability ranking, with an average monthly subscription cost of just $2 and a per-megabit rate of $0.83. While the country has faced years of political and economic turbulence, its broadband sector has managed to maintain strikingly low consumer-level pricing compared to continental peers. This affordability is partly the result of a pricing environment shaped by state policy, currency fluctuations, and the presence of multiple telecom operators competing in a constrained but highly active market. Despite broader instability, demand for internet access remains high, and service providers often adopt aggressive pricing to maintain customer loyalty and market share.

The backbone of Sudan’s connectivity lies in its access to regional and international bandwidth through undersea cable connections landing at the Red Sea coast, particularly via Port Sudan. Operators such as Sudatel, Zain Sudan, and MTN Sudan leverage these international gateways to deliver services inland, supported by terrestrial fiber routes that connect major cities like Khartoum and Omdurman. Unlike many African states where satellite links still dominate rural access, Sudan’s relative proximity to global submarine cables allows operators to secure wholesale capacity at competitive rates. This structural advantage translates into lower costs for end users, even though service quality can be inconsistent due to limited investment in network upgrades.

Affordability is also reinforced by Sudan’s broader policy framework, which emphasizes maintaining low tariffs on basic services to encourage digital adoption. The National Telecommunication Corporation (NTC) has pursued policies aimed at expanding broadband penetration, including licensing multiple operators to create competition and introducing tariff oversight mechanisms. At the same time, Sudanese innovators and small enterprises have taken advantage of cheap broadband to build digital services in education, mobile payments, and logistics. International organizations, recognizing both the challenges and opportunities, have also supported initiatives to extend rural connectivity through community-based projects. Together, these factors have ensured that despite economic headwinds, Sudan continues to lead Africa in broadband affordability, a position that reflects not only market competition but also structural advantages linked to its geographic location and policy direction.

We welcome your feedback. Kindly direct any comments or observations regarding this article to our Editor-in-Chief at [email protected], with a copy to [email protected].