In Summary

- Africa has made significant progress in financial inclusion, with rising account ownership and expanding digital payment adoption driving economic participation.

- Leading countries like Kenya, South Africa, and Mauritius showcase high access and mobile-money integration, while emerging players such as Rwanda, Ghana, and Nigeria are rapidly advancing.

- Deepening usage of credit, savings, and investment products remains key, highlighting the need for financial literacy, targeted policies, and fintech innovation to ensure inclusive economic growth.

Deep Dive!!

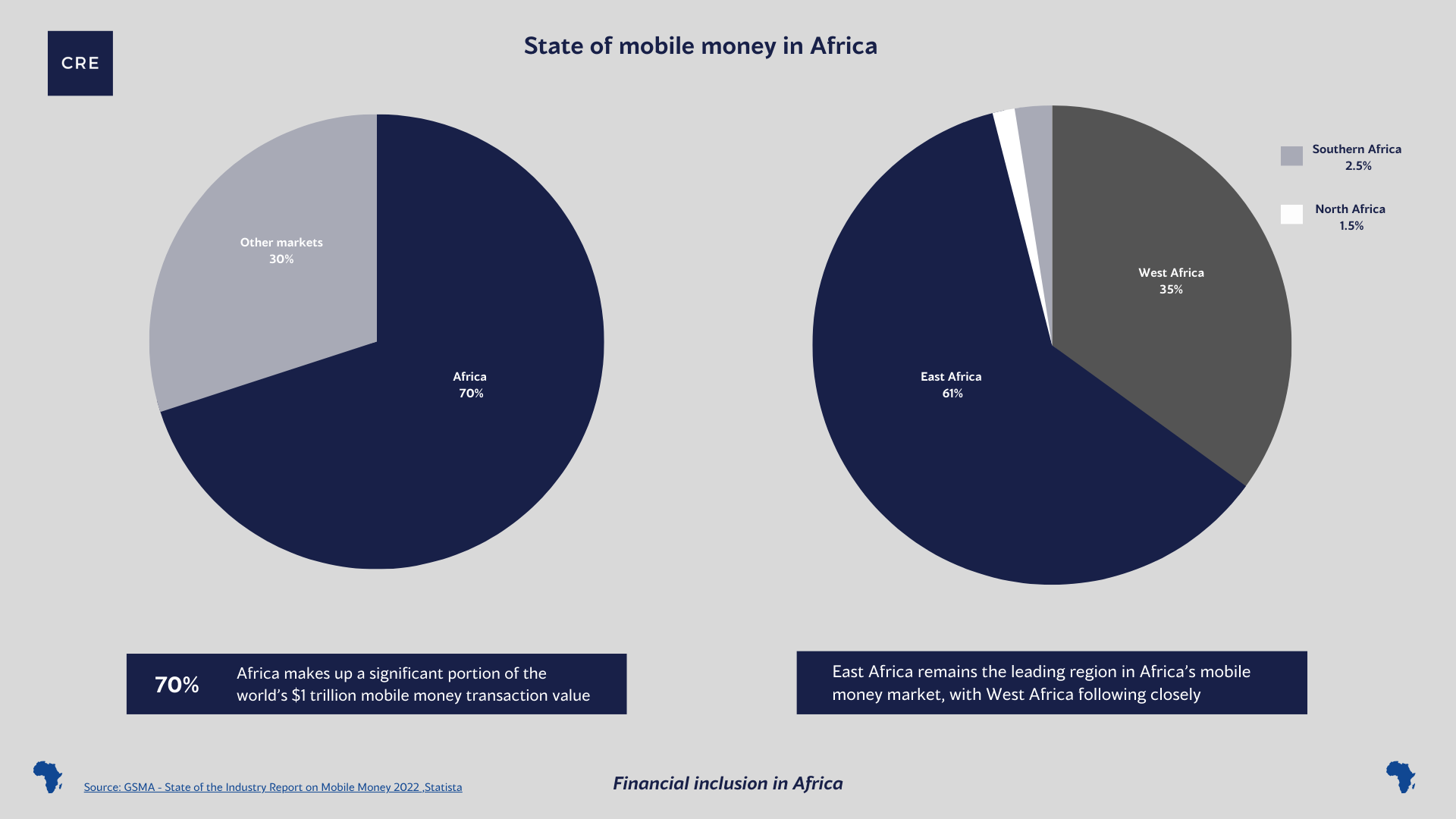

Monday, 10 November 2025– Financial inclusion has become a critical driver of economic growth and social development across Africa, enabling millions of individuals and businesses to participate in the formal financial system. Over the past decade, a combination of government policies, fintech innovation, and mobile-money adoption has transformed access to banking and digital financial services, bringing previously underserved populations into the mainstream economy. In 2025, African nations are demonstrating remarkable progress, with several countries achieving high account ownership rates and expanding the use of digital payment platforms, savings, and credit services. These advances not only facilitate everyday transactions but also create opportunities for entrepreneurship, investment, and economic resilience.

The landscape of financial inclusion in Africa is diverse, reflecting variations in infrastructure, regulatory frameworks, technological adoption, and population dynamics. Countries such as Kenya, South Africa, and Mauritius have set benchmarks in digital banking, mobile-money penetration, and formal account ownership, while emerging players like Rwanda, Ghana, and Nigeria are rapidly closing the gap through targeted policy initiatives and innovative fintech solutions. Measuring inclusion requires looking beyond account ownership to assess the depth of engagement, including savings behavior, access to credit, insurance, and investment products, as well as the ability of citizens to participate fully in the digital economy.

Understanding the current leaders and trends in African financial inclusion provides valuable insights for policymakers, investors, and development partners. By analyzing the countries that have achieved the strongest inclusion indices, identifying the enablers behind their success, and examining areas that require further development, stakeholders can better design strategies to promote inclusive growth across the continent. This article explores the Top 10 African Countries with the Strongest Financial Inclusion Index in 2025, highlighting achievements, challenges, and lessons that can inform efforts to create more equitable and accessible financial systems across Africa.

10. Zambia

Zambia has made notable strides in financial inclusion, particularly through the expansion of digital payment platforms and mobile money services. By 2024, approximately 72.7 % of adults in Zambia had a bank or mobile money account, a significant increase from around 49 % in 2021. This growth reflects both government initiatives to expand access to financial services and the rapid adoption of mobile technology in urban and peri-urban areas. Platforms like MTN Mobile Money and Airtel Money have played a critical role in bridging traditional banking gaps, allowing more Zambians to send and receive payments digitally.

Despite this progress, deepening financial inclusion remains a challenge in Zambia. While account ownership has risen sharply, actual usage of formal savings, credit, and investment products lags behind. Many users still rely primarily on mobile wallets for daily transactions rather than leveraging broader banking services such as loans, insurance, or long-term savings. Limited financial literacy, insufficient outreach in rural areas, and underdeveloped credit scoring systems continue to constrain the ability of individuals and small businesses to fully benefit from formal financial services.

Looking forward, Zambia’s financial inclusion trajectory will depend on targeted policies and ecosystem development. Strengthening regulatory frameworks for mobile money, expanding digital infrastructure into rural regions, and promoting financial literacy programs are key priorities. Additionally, partnerships between banks, fintechs, and government agencies can help channel formal credit to underserved populations, ensuring that the impressive gains in account ownership translate into meaningful economic empowerment. By addressing these gaps, Zambia has the potential not only to increase the number of account holders but also to foster a more resilient and inclusive financial system across the country.

9. Ghana

Ghana has emerged as a leading financial inclusion hub in West Africa, achieving approximately 81.2 % adult account ownership in 2024. This growth reflects concerted efforts by the government, regulators, and private sector players to expand access to banking services, particularly through digital channels. Initiatives such as the National Financial Inclusion and Development Strategy and partnerships with fintech companies have helped increase the reach of both traditional bank accounts and mobile wallets, making financial services more accessible to urban and rural populations alike.

The country’s digital banking ecosystem has grown rapidly, with mobile wallets and e-payment platforms facilitating seamless transactions for individuals and small businesses.MobileMoney Africa reportsthat the uptake of mobile-based banking solutions has been especially strong among younger populations and SMEs, enabling broader participation in the formal economy. This digital leap not only promotes convenience but also reduces reliance on cash, enhancing transparency and efficiency in financial transactions across the country.

Despite these achievements, deeper financial engagement remains a priority for Ghana. While account ownership is high, many users do not actively leverage formal savings, credit, or insurance products, limiting the full potential of financial inclusion. Expanding access to loans, microcredit, and investment opportunities, coupled with financial literacy programs, will be crucial in translating account ownership into meaningful economic empowerment. Strengthening these aspects will enable Ghana to not only maintain its leadership in West Africa but also drive sustainable growth and resilience across its financial ecosystem.

8. Namibia

Namibia has established itself as a notable performer in financial inclusion within Southern Africa, with account ownership levels hovering around 73 % according to recent data. This reflects a combination of stable economic conditions, widespread banking infrastructure, and government initiatives aimed at promoting access to formal financial services. Urban and peri-urban populations particularly benefit from the availability of bank branches, ATMs, and digital banking platforms, which facilitate everyday transactions and expand participation in the formal economy.

While Namibia’s mobile-money adoption is not as high as in East African leaders like Kenya or small island economies like Mauritius, the country compensates with a robust regulatory environment and strong institutional support. The government and central bank have implemented frameworks that promote consumer protection, financial stability, and secure digital payments. These measures help build trust in formal financial systems, encouraging more citizens to open and maintain accounts with banks and financial institutions, even if they do not yet fully exploit mobile money for transactions.

Going forward, Namibia’s path to deeper financial inclusion will likely involve expanding digital payment solutions and enhancing financial literacy. Encouraging mobile-money services and fintech innovation could help reach rural communities and underserved populations, bridging gaps in access. Additionally, strengthening credit and savings products, alongside programs targeting small businesses and informal sector workers, will be key to converting account ownership into meaningful financial engagement. With its strong regulatory and institutional foundations, Namibia is well-positioned to consolidate gains and become a leading model for inclusive finance in Southern Africa.

7. Uganda

Uganda has made significant strides in financial inclusion, with recent surveys indicating that approximately 68 % of adults hold a formal bank or mobile-money account. This achievement places the country ahead of many of its regional peers, reflecting the combined impact of government initiatives, regulatory support, and private sector innovation. The proliferation of mobile-money services, particularly platforms like MTN Mobile Money and Airtel Money, has been instrumental in extending financial access to rural areas and informal sector participants who traditionally lacked access to banking services.

Uganda’s mobile-money ecosystem has been a driving force behind its inclusion progress, enabling millions to perform digital transactions, receive remittances, and pay bills electronically. The convenience, security, and low cost of these services have encouraged widespread adoption, making mobile-money accounts more prevalent than traditional bank accounts in many communities. This technology has not only improved day-to-day financial transactions but has also facilitated greater integration of informal economic actors into the formal financial system, strengthening overall economic resilience.

Despite these gains, deep financial engagement remains limited. While account ownership is robust, the uptake of formal savings, loans, and credit products remains comparatively low, highlighting a gap between access and usage. Addressing these challenges requires targeted interventions, including financial literacy programs, expanded credit facilities, and products tailored to low-income and rural populations. By enhancing the depth of inclusion, ensuring that individuals and businesses not only hold accounts but actively use them for savings, borrowing, and investment, Uganda can strengthen its financial ecosystem and unlock broader economic benefits for its citizens.

6. Rwanda

Rwanda has emerged as a notable financial inclusion success story in Africa, with significant progress in account ownership and access to digital financial services. By 2025, the country reports an adult account ownership rate of approximately 83 %, reflecting years of targeted government policies, regulatory support, and public-private partnerships aimed at expanding access to banking and mobile-money services. Programs under the National Strategy for Transformation, combined with the efforts of Rwanda’s central bank, have created a conducive environment for both traditional banks and fintech startups to reach underserved populations across urban and rural areas.

A key driver of Rwanda’s success is its robust mobile-money ecosystem, which has enabled widespread adoption of digital payments, remittances, and savings platforms. Providers like MTN Mobile Money and Airtel Money have made financial services accessible to communities that previously lacked proximity to bank branches. The government’s push for digitization, including cashless payments for public services and utility bills, has further accelerated uptake, making Rwanda one of the fastest-growing digital financial markets in the region. These innovations not only simplify everyday transactions but also promote transparency, security, and inclusion in economic activities.

Despite strong account ownership, Rwanda faces challenges in deepening financial engagement. While mobile-money usage is high, uptake of formal credit, savings, and investment products remains relatively limited, particularly among low-income households and rural populations. Expanding financial literacy programs, developing microfinance and tailored credit products, and fostering fintech innovation will be essential to convert account access into meaningful economic empowerment. With its strong institutional framework and supportive policy environment, Rwanda is well-positioned to consolidate its financial inclusion gains and serve as a model for other African nations seeking inclusive digital financial growth.

5. Mauritius

Mauritius stands out as a leading financial inclusion performer in Africa, with approximately 89.6 % of adults holding a bank account in 2024. This places the island nation among the top countries on the continent in terms of access to formal financial services. A combination of high literacy rates, stable economic conditions, and asophisticated banking infrastructureunderpins this achievement. The widespread availability of banking branches, ATMs, and online banking platforms ensures that both urban and rural populations can access and manage financial accounts with relative ease.

The formal financial sector in Mauritius is robust, characterized by well-capitalized banks, strong regulatory oversight, and consumer protection mechanisms that foster trust and participation. While account ownership is extremely high, the uptake of mobile money and alternative digital financial services remains comparatively modest. Unlike East African countries such as Kenya, where mobile-money penetration drives everyday transactions, Mauritian citizens predominantly rely on traditional banking channels for payments, savings, and investments. Nevertheless, the strong institutional framework provides a solid foundation for expanding digital financial services in the coming years.

Looking ahead, Mauritius has the potential to deepen financial inclusion by enhancing credit access and promoting diversified financial products. Initiatives to expand small business lending, microfinance, and insurance penetration could enable more citizens to leverage formal financial systems for economic advancement. Additionally, promoting fintech adoption and mobile-based solutions can complement the existing infrastructure, particularly for younger and tech-savvy populations. By building on its strong account ownership base, Mauritius is well-positioned to maintain its leadership in financial inclusion while fostering broader economic empowerment across the nation.

4. South Africa

South Africa has long been recognized as a continental leader in financial inclusion, with surveys indicating that up to 97 % of adults hold a bank or formal financial account. This high level of account ownership reflects the country’s well-developed banking infrastructure, extensive branch networks, and widespread availability of ATMs and online banking services. The formal financial system benefits from strong regulatory oversight, robust consumer protection laws, and high levels of financial literacy, all of which create an environment conducive to broad participation.

Despite these impressive figures, financial inclusion in South Africa faces challenges in terms of depth and equity. While most adults technically have accounts, the use of financial services by underserved populations, particularly in rural areas and informal settlements, remains limited. Mobile-only accounts and digital wallets are gaining traction, but adoption is uneven, and many low-income individuals still struggle to access credit, savings, and insurance products. This gap between account ownership and meaningful engagement highlights the need for targeted interventions that go beyond simply opening accounts.

To strengthen inclusion, South Africa must focus on enhancing usage and financial capability among marginalized groups. Expanding access to microloans, tailored savings products, and affordable insurance can help underserved populations fully benefit from the formal financial system. Additionally, fintech innovations and mobile banking solutions can bridge geographic and socioeconomic barriers, bringing financial services closer to rural and low-income communities. By addressing these challenges, South Africa can not only maintain its position as a leader in account access but also ensure that financial inclusion translates into tangible economic empowerment across all segments of society.

3. Nigeria

Nigeria has emerged as one of Africa’s fastest-growing financial inclusion markets, driven by a combination of government initiatives, fintech innovation, and mobile-money adoption. As of 2025, Nigeria boasts approximately 456 registered fintech and AI-enabled financial services companies, which have significantly expanded access to banking services, particularly for the previously unbanked populations. Programs such as the National Financial Inclusion Strategy and partnerships between commercial banks and mobile operators have helped increase account ownership and digital payment adoption across urban and rural areas.

Nigeria’s mobile-money and digital banking ecosystem has played a pivotal role in bridging financial access gaps. Platforms like Paga, Flutterwave, and Opay have enabled millions of Nigerians to send and receive money, pay bills, and conduct e-commerce transactions without relying on traditional bank branches. The rise of agent banking and USSD-based services has further expanded inclusion to rural communities, ensuring that financial services are accessible even to those without smartphones or internet connectivity. This ecosystem not only supports daily transactions but also lays the groundwork for broader adoption of savings, credit, and insurance products.

Despite these advances, Nigeria faces challenges in deepening financial engagement beyond account ownership. While a growing number of Nigerians now have access to financial services, meaningful use of formal savings, credit, and investment products remains limited for many low-income households and micro-entrepreneurs. Enhancing financial literacy, expanding microcredit and insurance offerings, and integrating fintech solutions with traditional banking will be essential for translating access into empowerment. By addressing these gaps, Nigeria can consolidate its position as a leading financial inclusion market in Africa, fostering economic growth and resilience across diverse populations.

2. Kenya

Kenya has firmly established itself as a continental leader in financial inclusion, with approximately 90.1 % of adults holding a bank or mobile-money account in 2024. This remarkable achievement reflects the country’s long-standing commitment to expanding access to financial services, supported by a combination of regulatory initiatives, private sector innovation, and widespread mobile connectivity. The government and financial institutions have worked together to reduce barriers to account ownership, making it easier for individuals across both urban and rural areas to participate in the formal financial system.

A cornerstone of Kenya’s success is its robust mobile-money ecosystem, led by M Pesa, which has revolutionized the way millions of Kenyans transact. With 93 % adult mobile-phone penetration and 89 % of adults engaging in digital payments, the country has created a vibrant digital financial landscape that extends beyond traditional banking. Mobile-money platforms facilitate everyday transactions, bill payments, remittances, and e-commerce, effectively integrating informal sector participants into the formal economy. This widespread adoption has not only improved convenience and efficiency but also strengthened financial resilience among households and small businesses.

Despite these impressive gains, Kenya faces the ongoing challenge of deepening financial engagement beyond account access. While most adults hold accounts, the uptake of savings, loans, insurance, and investment products varies across different income groups and regions. Expanding the availability of tailored financial products, enhancing financial literacy programs, and integrating fintech solutions with traditional banking channels will be critical to ensure that financial inclusion translates into real economic empowerment. By focusing on these areas, Kenya can consolidate its leadership position and fully leverage its mobile-money ecosystem to drive inclusive growth and long-term economic resilience.

1. Seychelles

Seychelles has established itself as one of Africa’s most financially inclusive countries, with a high rate of account ownership among adults, estimated at over 88 % in 2024. This achievement is supported by the nation’s strong banking infrastructure, high literacy levels, and a relatively small population, which allows financial institutions to efficiently reach citizens across both urban and rural areas. The government’s commitment to promoting financial access through supportive policies and digital initiatives has further reinforced Seychelles’ position as a leader in the region.

A key factor driving Seychelles’ financial inclusion is its well-developed formal financial sector, which provides a wide range of banking services including savings, payments, and investment products. While mobile-money adoption is not as pervasive as in East Africa, the country has leveraged digital banking platforms and online services to facilitate seamless transactions and reduce reliance on cash. These services cater to both individuals and businesses, enabling greater economic participation and enhancing financial security across the population.

Despite high account ownership, Seychelles faces opportunities to deepen financial engagement through increased uptake of credit, microloans, and insurance products. Expanding financial literacy initiatives and encouraging the use of digital financial services among underserved populations will be crucial to converting account access into meaningful economic empowerment. With its strong institutional foundations and innovative financial ecosystem, Seychelles is well-positioned to maintain its leadership in financial inclusion while fostering sustainable economic growth and resilience for its citizens.

We welcome your feedback. Kindly direct any comments or observations regarding this article to our Editor-in-Chief at [email protected], with a copy to [email protected].